How Catastrophe Bonds Work

Infographic with Example

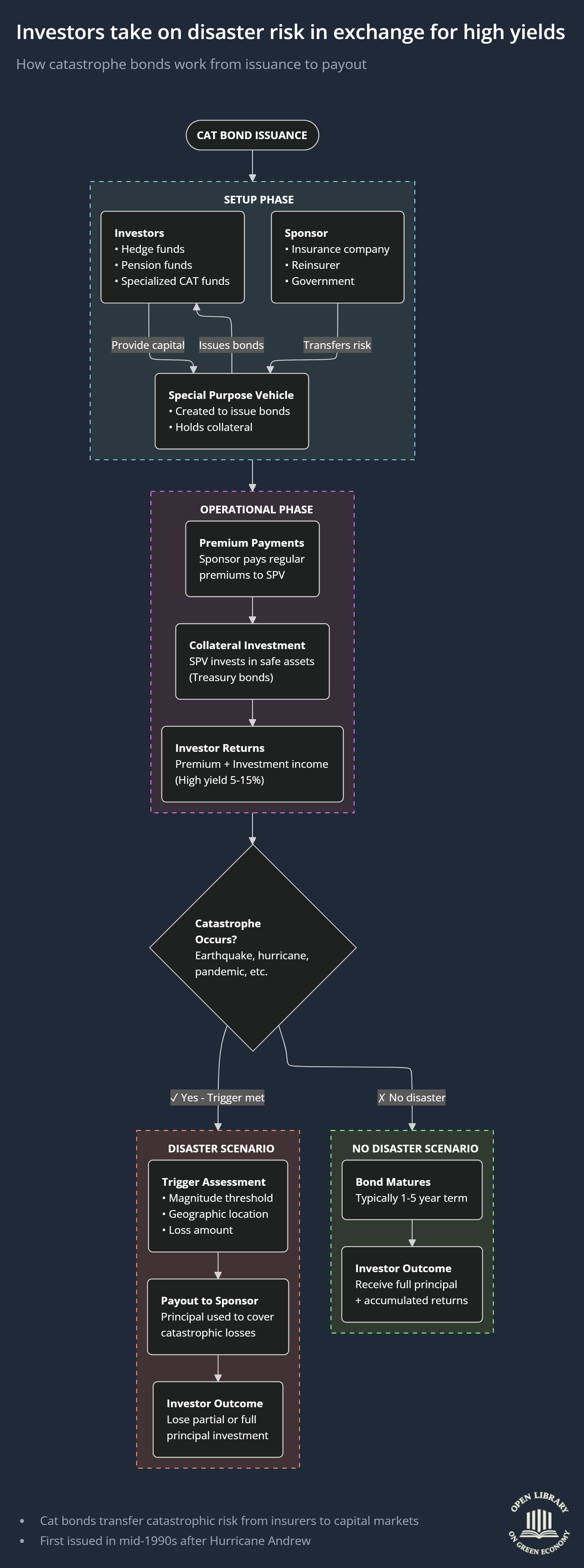

This chart explains how catastrophe bonds, usually called cat bonds, work from issuance to final outcome. The core idea is simple, investors earn high yields by taking on the risk of rare but severe disasters, while insurers or governments transfer that disaster risk away from their balance sheets.

The process starts with cat bond issuance. A sponsor initiates the transaction. The sponsor can be an insurance company, a reinsurance firm, or a government that wants protection against events like earthquakes, hurricanes, floods, or pandemics. Instead of buying traditional reinsurance, the sponsor turns to capital markets.

During the setup phase, investors such as hedge funds, pension funds, and specialised catastrophe bond funds commit capital. This money does not go directly to the sponsor. Instead, it is placed into a special purpose vehicle, or SPV. The SPV is created only for this bond. Its role is to issue the bonds, hold the investor capital as collateral, and act as a firewall between investors and the sponsor.

Once the SPV is set up, two things happen in parallel. Investors provide capital to the SPV by buying the bonds. The sponsor transfers catastrophe risk to the SPV by agreeing that if a defined disaster occurs, the SPV will release funds to cover losses. This is how risk moves from insurers or governments to investors.

Next comes the operational phase. Throughout the life of the bond, the sponsor pays regular premium payments to the SPV. These premiums are similar to insurance premiums. At the same time, the SPV invests the collateral in very safe assets, usually government treasury securities. The combination of premium payments and investment income is what generates investor returns. Because investors are taking on disaster risk, the yields are high, typically in the range of five to fifteen percent.

Then the critical question arises. Does a catastrophe occur during the bond term. The bond includes very specific trigger conditions, such as the magnitude of an earthquake, the wind speed of a hurricane, the geographic location, and the size of insured losses.

If no qualifying disaster occurs, the bond simply runs to maturity, usually after one to five years. Investors receive their full principal back along with all accumulated interest. This is the best case scenario for investors and the most expensive outcome for the sponsor, since premiums were paid but no payout was needed.

If a qualifying disaster does occur and the trigger conditions are met, the bond enters the disaster scenario. An independent assessment confirms whether the trigger thresholds are crossed. If they are, the SPV releases some or all of the collateral to the sponsor to cover catastrophic losses. In this case, investors lose part or all of their principal. This loss is not a default. It is the core feature of the product.

A real world example helps clarify this. After major hurricanes in the United States, insurance companies often issue hurricane cat bonds tied to wind speed or modeled loss levels. If no major hurricane hits the covered region during the bond term, investors earn high yields and get their capital back. If a major hurricane strikes and exceeds the trigger thresholds, investor capital is used immediately to help insurers pay claims, reducing financial strain on the insurance system.

The chart shows why cat bonds exist. They move extreme disaster risk from insurers and governments into capital markets, where investors are willing to bear it in exchange for attractive returns. At the same time, they provide fast, reliable funding after catastrophic events without relying on emergency government bailouts.