The EU Taxonomy Explained - From Policy to Practice

Implementing the EU Taxonomy for Sustainable Finance

Introduction

The European Union Taxonomy for Sustainable Activities ("EU Taxonomy") represents one of the most significant and ambitious regulatory frameworks in the global sustainable finance landscape. Established as part of the European Green Deal and the broader EU Sustainable Finance Action Plan, this classification system aims to redirect capital flows toward sustainable investments by providing clear definitions of what constitutes environmentally sustainable economic activities. As the world grapples with the urgent need to transition to a low-carbon economy and address multiple ecological crises, the EU Taxonomy serves as a pioneering tool that may well become the gold standard for sustainable finance globally.

Historical Context and Development

The EU Taxonomy emerged from a recognition that achieving climate neutrality by 2050 would require mobilising unprecedented financial resources. The High-Level Expert Group on Sustainable Finance (HLEG), established in 2016, identified the lack of a common language and clear definitions as major barriers to scaling up sustainable finance. Following HLEG's recommendations, the European Commission established the Technical Expert Group on Sustainable Finance (TEG) in 2018 to develop the taxonomy.

The Taxonomy Regulation (Regulation (EU) 2020/852) entered into force in July 2020, establishing the framework for the EU Taxonomy. This was followed by delegated acts specifying technical screening criteria for various economic activities. The first delegated act on climate objectives was adopted in June 2021, with implementation beginning in January 2022.

Main Components of the EU Taxonomy

The Four Essential Conditions

For an economic activity to qualify as environmentally sustainable under the EU Taxonomy, it must satisfy all four of the following conditions:

Substantial Contribution: The activity must contribute substantially to at least one of the six environmental objectives (discussed below). This means that the activity must either directly enable environmental improvements or provide the means for other activities to do so.

Do No Significant Harm (DNSH): The activity must not significantly harm any of the other environmental objectives. This principle ensures that progress toward one environmental goal does not come at the expense of others.

Minimum Safeguards: The activity must be carried out in compliance with minimum social safeguards specified by the EU. These are aligned with international standards including the OECD Guidelines for Multinational Enterprises, the UN Guiding Principles on Business and Human Rights, the International Labour Organization's core conventions, and the International Bill of Human Rights.

Technical Screening Criteria: The activity must comply with technical screening criteria established by the European Commission through delegated acts. These criteria provide specific thresholds and requirements that determine when an activity makes a substantial contribution to an environmental objective and when it does not cause significant harm.

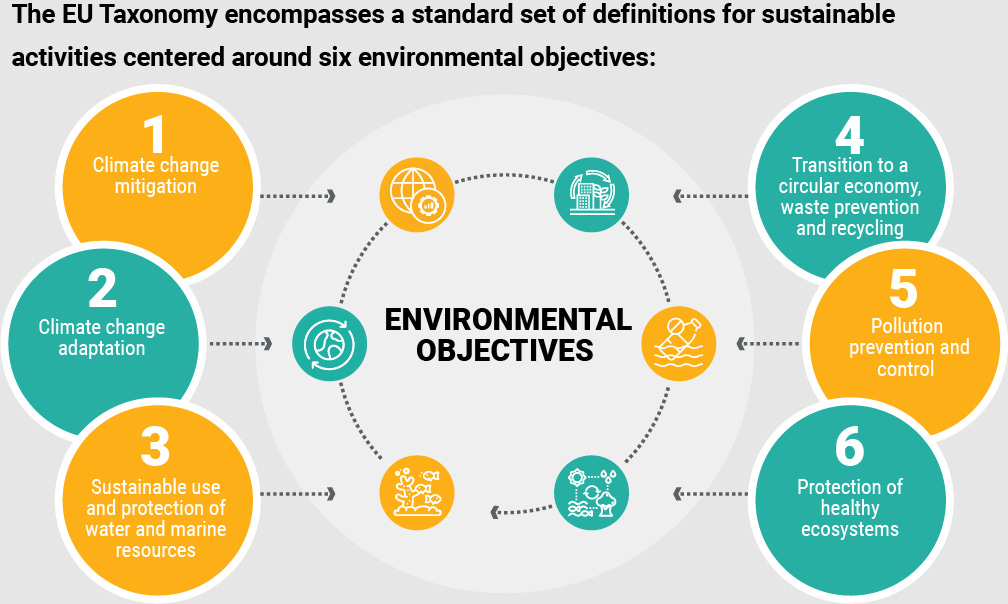

The Six Environmental Objectives

The EU Taxonomy defines six environmental objectives toward which economic activities should contribute:

Climate Change Mitigation: Activities that contribute to the stabilisation of greenhouse gas concentrations in the atmosphere at a level that prevents dangerous anthropogenic interference with the climate system. This includes reducing or preventing greenhouse gas emissions or enhancing greenhouse gas removals.

Climate Change Adaptation: Activities that reduce the adverse impacts of the current and expected future climate on an economic activity, people, nature, or assets, or prevent the increase or shifting of adverse impacts.

Sustainable Use and Protection of Water and Marine Resources: Activities that contribute to achieving good status of water bodies, including surface waters, groundwaters, and marine waters, or to preventing their deterioration when already in good status.

Transition to a Circular Economy: Activities that contribute to waste prevention, reuse, and recycling, including preventing or reducing waste generation, improving resource efficiency, and transitioning to circular business models.

Pollution Prevention and Control: Activities that contribute to preventing or reducing emissions of pollutants into air, water, or land, other than greenhouse gases.

Protection and Restoration of Biodiversity and Ecosystems: Activities that contribute to protecting, conserving, or restoring biodiversity or to achieving the good condition of ecosystems, or to protecting ecosystems that are already in good condition.

Implementation and Disclosure Requirements

Phased Approach

The EU has adopted a phased approach to implementing the Taxonomy:

Phase 1 (2022): Companies and financial market participants subject to the Non-Financial Reporting Directive (NFRD) began disclosing how and to what extent their activities are aligned with the Taxonomy in relation to climate change mitigation and adaptation objectives.

Phase 2 (2023 onwards): Disclosures expanded to cover all six environmental objectives, and more detailed reporting requirements came into effect.

Corporate Sustainability Reporting

Under the Corporate Sustainability Reporting Directive (CSRD), which replaces and expands the scope of the NFRD, approximately 50,000 companies in the EU will need to report on their Taxonomy alignment. Companies must disclose:

The proportion of their turnover derived from products or services associated with Taxonomy-aligned economic activities.

The proportion of their capital expenditure and operating expenditure related to assets or processes associated with Taxonomy-aligned economic activities.

Financial Product Disclosures

Financial market participants offering financial products in the EU must disclose:

How and to what extent they have used the Taxonomy in determining the sustainability of the underlying investments.

The proportion of underlying investments that are Taxonomy-aligned, expressed as a percentage.

For products that promote environmental characteristics (Article 8 products under SFDR) or have sustainable investment as their objective (Article 9 products under SFDR), additional detailed disclosures are required.

The Taxonomy in Practice: Types of Activities

The EU Taxonomy recognises different types of activities based on their environmental performance:

Green Activities

These are activities that make a substantial contribution to one or more environmental objectives without significantly harming any others. They include:

Already Low-carbon Activities: Activities that are already compatible with a climate-neutral economy (e.g., zero-emission transport, near-zero carbon electricity generation).

Transitional Activities: Activities for which low-carbon alternatives are not yet available but that support the transition to a climate-neutral economy (e.g., efficient manufacturing techniques that reduce emissions significantly compared to industry averages).

Enabling Activities: Activities that enable substantial contribution to one or more objectives in other sectors (e.g., manufacturing components for renewable energy technologies).

Significant Harm Activities

Activities that significantly harm environmental objectives and cannot be made compatible with the Taxonomy's requirements (e.g., power generation from solid fossil fuels).

Global Influence and Policy Implications

International Harmonisation Efforts

The EU Taxonomy has sparked similar initiatives worldwide:

China has developed its own taxonomy for green finance.

The International Platform on Sustainable Finance (IPSF), co-founded by the EU and involving major economies like China, India, and Canada, works to harmonise taxonomies globally.

The emergence of the "Common Ground Taxonomy" between EU and China represents an important step toward international convergence.

Policy Influence Beyond Sustainable Finance

The Taxonomy influences broader policy areas:

Green Public Procurement: GPP is a strategy where public bodies prioritise purchasing goods, services, and works with minimal environmental impact throughout their life cycle, aiming to reduce carbon emissions and promote sustainability. Member states are increasingly aligning procurement criteria with the Taxonomy.

State Aid and Recovery Funds: The Recovery and Resilience Facility requires member states to allocate at least 37% of expenditure to climate objectives, with the Taxonomy providing guidance.

Monetary Policy: The European Central Bank is exploring how to incorporate the Taxonomy into its operations.

Challenges and Controversies

Technical Complexity and Data Availability

The technical screening criteria are complex and detailed, posing implementation challenges for companies and investors. Data availability and quality remain significant hurdles, particularly for smaller companies and for activities outside the EU.

Contentious Classifications

Some classification decisions have generated controversy, particularly regarding:

Nuclear Energy: Included as a transitional activity under specific conditions, despite objections from several member states.

Natural Gas: Classified as transitional under certain conditions, which some critics argue undermines climate objectives.

Forestry and Bioenergy: Criteria for these sectors have faced criticism from both industry and environmental groups.

Evolving Framework

The Taxonomy is not static but will evolve with technological developments and scientific understanding. The Platform on Sustainable Finance continues to advise the Commission on updates to technical screening criteria and potential extensions to the framework.

The Social Taxonomy and Future Directions

While the current EU Taxonomy focuses on environmental objectives, work is underway to develop a Social Taxonomy that would define socially sustainable activities. This would address aspects such as:

Fair working conditions.

Inclusive and accessible products and services.

Sustainable communities and societies.

Additionally, discussions are ongoing about a potential extension to cover:

Activities with no significant impact on environmental objectives.

Activities that significantly harm environmental sustainability ("brown taxonomy").

Implications for Different Stakeholders

For Companies

Need to assess activities against Taxonomy criteria and potentially adapt business strategies.

Disclosure requirements creating new reporting burdens but also opportunities for demonstrating sustainability credentials.

Access to capital may increasingly depend on Taxonomy alignment.

For Financial Institutions

Required to assess and disclose Taxonomy alignment of portfolios.

Need to develop new data collection processes and evaluation methodologies.

Opportunity to develop new green financial products with clear sustainability credentials.

For Investors

Improved transparency enabling more informed investment decisions.

Reduced risk of greenwashing in financial products, where organisations exaggerate their environmental credentials, among so-called eco-friendly investment products.

Potential impact on asset valuations as capital flows toward Taxonomy-aligned activities.

For Policymakers

Benchmark for designing green policies and incentives.

Tool for monitoring progress toward environmental objectives.

Framework for international cooperation on sustainable finance.

Conclusion

The EU Taxonomy provides an unprecedented level of clarity and transparency to the sustainable finance market. As climate change and environmental degradation continue to threaten global prosperity and security, tools like the Taxonomy will be essential for mobilising capital at the scale and speed required for a sustainable transition.

By establishing a common language for sustainable activities, the EU Taxonomy helps bridge the gap between climate commitments and financial decision-making. Its influence extends far beyond the EU's borders, potentially setting a global standard for sustainable finance classification. For stakeholders across the spectrum—from companies and investors to policymakers and citizens—understanding and engaging with the Taxonomy will be increasingly important in navigating the transition to a more sustainable economy.