What are Blue Bonds?

Understanding Blue Bonds and Sustainable Ocean Finance, Market Growth & Trends, Standards & Frameworks, Stakeholder Ecosystem, Corporate Innovations, Blue Carbon, Infographics, and Recommendations

The global ocean economy generates roughly $2.5 trillion in annual value and supports the livelihoods of more than three billion people. This vast system underpins international trade, food security, and climate regulation through industries ranging from small-scale fisheries to offshore renewable energy. Yet despite its economic importance, the ocean faces what experts call a triple planetary crisis. Climate change, biodiversity loss, and pollution are degrading marine ecosystems at an alarming rate.

Meeting Sustainable Development Goal 14 (Life Below Water), alone, requires an estimated $175 billion per year through 2030. Between 2015 and 2019, actual investment in ocean health totaled just $10 billion. This leaves a funding gap of roughly 90%. Traditional public funding cannot close this gap alone, which has led the financial sector to develop innovative instruments that can mobilise private capital for ocean conservation and sustainable maritime industries.

Blue bonds represent one of the most promising approaches to this problem. These specialised debt securities direct capital specifically toward projects that restore marine ecosystems, build coastal resilience, and support sustainable ocean industries. Since the Seychelles issued the world’s first sovereign blue bond in 2018, the market has grown rapidly. What began as small pilot projects has evolved into sophisticated financial structures that include corporate benchmarks, short-term repo transactions, and complex debt-for-nature swaps.

What Blue Finance Actually Means

Blue finance emerged from the broader sustainable debt market, which started with the first green bonds in 2007 and 2008. While green bonds have dominated the environmental, social, and governance (ESG) landscape, marine environments present challenges that require more focused approaches. The term “blue finance” refers to any financial instrument that channels capital toward the sustainable use and protection of marine and freshwater ecosystems. The goal is to align economic growth with the preservation of natural capital in aquatic systems.

The Structure of a Blue Bond

A blue bond functions exactly like a conventional bond. Governments, multilateral development banks, or corporations issue them to raise capital. Investors provide that capital in exchange for periodic interest payments (called coupons) and the return of their principal when the bond matures. What makes these bonds “blue” is how the proceeds are used. The issuer must dedicate funds exclusively to projects that deliver positive environmental and social benefits for aquatic environments.

To earn the blue designation, bonds must follow established market standards. Most follow the International Capital Market Association’s Green Bond Principles, which require transparency across four areas, viz., how proceeds will be used, how projects are selected, how funds are managed, and how impact is reported. Increasingly, blue bonds are also expected to contribute directly to SDG 14 and SDG 6 (Clean Water and Sanitation).

How Blue Bonds Differ from Green Bonds

Blue bonds are essentially a specialised subset of green bonds focused on aquatic themes. However, ocean ecosystems have specific characteristics that require different criteria. For example, ocean health depends heavily on what happens upstream in freshwater systems. Nutrients and plastics that rivers carry downstream are major drivers of coastal dead zones and oceanic pollution. This connectivity means blue finance needs specialised standards that capture the relationship between land and sea.

The differences become clearer when you compare typical projects. Green bonds might fund solar farms, electric vehicle infrastructure, or energy-efficient buildings. Blue bonds, by contrast, fund sustainable fisheries, aquaculture improvements, plastic waste reduction programs, or marine spatial planning initiatives. Green bonds target SDGs related to energy, cities, and land use. Blue bonds focus on life below water and clean water access.

The Water Cycle Approach

An important change occurred in 2024 and 2025. Financial institutions like Natixis and the International Finance Corporation began advocating for a more holistic view that integrates the entire hydrological cycle into blue finance. Traditionally, blue finance focused strictly on marine assets. But recognising that ocean health is inseparable from what happens on land, practitioners have expanded the scope to include freshwater management and wastewater treatment.

This evolution makes practical sense. It allows the blue bond market to tap into broader infrastructure financing for sanitation and urban water security, particularly in emerging markets where water stress creates acute social and economic risks. By acknowledging that rivers, lakes, and coastal wetlands are all connected to ocean health, blue finance can address problems more comprehensively.

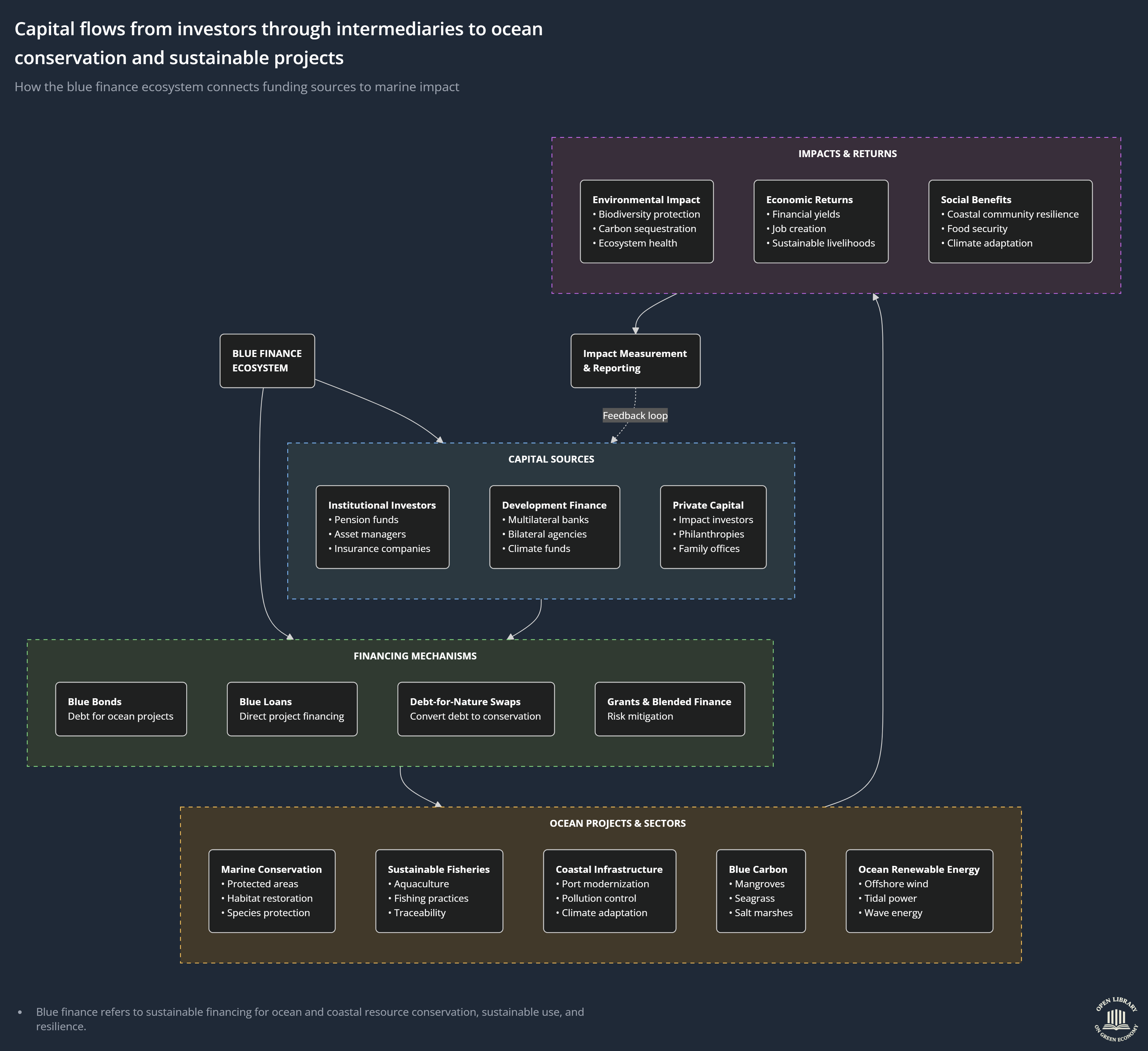

How Blue Finance Works in Practice

Blue finance uses several mechanisms to connect institutional investors seeking returns with conservation projects that need patient, long-term capital.

Use-of-Proceeds Versus Sustainability-Linked Structures

Most blue bonds issued so far follow what’s called a use-of-proceeds model. The issuer legally commits to spending the raised capital on a specific list of eligible blue projects. This structure gives investors clear visibility into where their money goes and what environmental impact it creates.

Sustainability-linked bonds work differently. These are general-purpose bonds where the financial terms adjust based on whether the issuer meets predefined sustainability targets. For instance, a seafood company might issue a bond where the interest rate drops if it achieves 100% certification for sustainable aquaculture within five years. This structure offers more flexibility for companies trying to transition their entire operations, but it has faced criticism for weak penalty structures. As a result, issuance of sustainability-linked bonds declined in 2024 compared to other categories.

Overcoming Credit Barriers Through Blended Finance

Many coastal developing nations that could benefit most from blue bonds face a structural problem. Their credit ratings make it difficult or impossible to access international capital markets at affordable interest rates. Blended finance structures address this by combining public or philanthropic capital with private investment to reduce risk.

Several tools make this possible. Partial credit guarantees from institutions like the World Bank or Asian Development Bank cover a portion of the principal or interest, which lowers default risk and improves the bond’s credit rating. Concessional loans from organisations like the Global Environment Facility provide low-interest capital that can subsidise coupon payments, reducing the effective interest rate for the issuer. Political risk insurance from entities like the U.S. International Development Finance Corporation protects investors against non-commercial risks such as currency problems or government contract breaches.

The Seychelles issuance demonstrates how effective these tools can be. Credit enhancements allowed the sovereign to save over $8 million in interest charges over ten years, effectively lowering the borrowing cost by roughly 5% per year.

Blue Repos and Blue Loans

The blue finance market continues to innovate. In March 2025, Banco do Brasil issued a $95 million blue repo transaction with Natixis. A repo, or repurchase agreement, is essentially a short-term collateralised loan. This transaction used capital to finance water and sanitation portfolios in Brazil. It shows that blue finance can adapt to short-term liquidity management needs, not just long-term project financing.

Blue loans have also emerged as an important instrument, particularly for private institutions. Since 2020, the International Finance Corporation has provided over $2 billion in blue loans supporting plastic recycling and water security projects. These function like blue bonds but typically involve private bilateral agreements between a borrower and a financial institution. They follow the Green Loan Principles rather than bond market standards.

Standards and Frameworks That Govern the Market

Maintaining market integrity requires clear standards. Without them, the market faces the risk of “bluewashing,” where financial products are misleadingly labeled as environmentally friendly.

The Sustainable Blue Economy Finance Principles

Launched in 2018 and hosted by the UN Environment Programme Finance Initiative, these 14 principles provide the foundation for how the finance sector engages with ocean issues. They offer a high-level framework for banks, insurers, and investors to align their activities with SDG 14. The principles emphasise three core approaches. Being protective (actively restoring marine health), being compliant (respecting regional frameworks and laws), and being risk-aware (incorporating long-term environmental assessments into decision-making).

ICMA and IFC Guidelines

The International Capital Market Association manages the most widely used standards in the sustainable bond market. In 2024, 93% of sustainable bond issuances referenced ICMA guidelines. In 2023, ICMA collaborated with the IFC, Asian Development Bank, UNEP FI, and the UN Global Compact to release a practitioner’s guide specifically for blue economy bonds. This guide provides explicit eligibility criteria for blue projects, suggests key performance indicators, and showcases examples of best practices.

The IFC’s Guidelines for Blue Finance, updated to Version 2.0 in 2025, offer even more detailed guidance. The updated framework expanded coverage to include water security (efficient supply and wastewater reuse), circular economy approaches (plastic recycling and waste reduction in river basins), shipping decarbonisation and sustainable port infrastructure, and marine conservation including blue carbon ecosystems.

Regional Standards and Their Importance

Regional taxonomies play a critical role in reducing transaction costs and building investor confidence. In Europe, the EU Taxonomy has set high standards for data quality, forcing issuers to improve transparency or face penalties for greenwashing. In Asia, the ASEAN Green Bond Standards require 100% allocation to eligible projects and explicitly exclude fossil-fuel-linked activities. This provides a more prescriptive framework than the voluntary international principles. Japan’s Green Bond Guidelines and China’s 2022 Green Bond Principles add further regional alignment by requiring consistency with national environmental catalogues.

These regional standards matter because they create consistency within major markets. When issuers know exactly what qualifies and what doesn’t, the cost and complexity of bringing a bond to market decreases.

Market Growth and Current Trends

The blue bond market remains small compared to the broader green bond sector, but it has shown resilience and steady growth.

Issuance Volumes and Market Development

Since 2018, the number of blue-labeled transactions has increased each year. In 2023, 16 labeled blue bonds raised $4.79 billion globally. In 2024, the number of issuances grew to 22, though total volume was lower at approximately $3.22 billion. This shift reflects more issuers entering the market with smaller, more targeted transactions. By the first half of 2025, blue bonds recorded the fastest year-on-year growth in market share relative to other sustainable bond categories, signaling rising investor interest in ocean-related sustainability.

The Greenium and Market Maturity

The term “greenium” refers to a yield discount that issuers of sustainable bonds pay compared to conventional bonds. In simpler terms, issuers can borrow at slightly lower interest rates because investor demand for sustainable assets often exceeds supply. This premium has been a notable feature of the ESG market for years. However, market data from 2024 suggests the greenium is shrinking as the market matures and supply increases.

Regional Dynamics

Europe remains the primary driver of sustainable finance, accounting for 51.7% of green bonds issued in 2024. However, Asia-Pacific is the fastest-growing region for blue finance. In 2024, Asian corporate sustainable bond issuance was four times larger than during the 2015-2019 period. China and Japan dominate this market, with Chinese green bonds representing 80% of corporate sustainable issuance in the country. Meanwhile, the United States experienced an ESG backlash in 2024, leading some issuers to pause their sustainable bond activities.

Case Studies

Sovereign blue bonds serve as powerful models for how coastal nations can align environmental commitments with long-term fiscal needs.

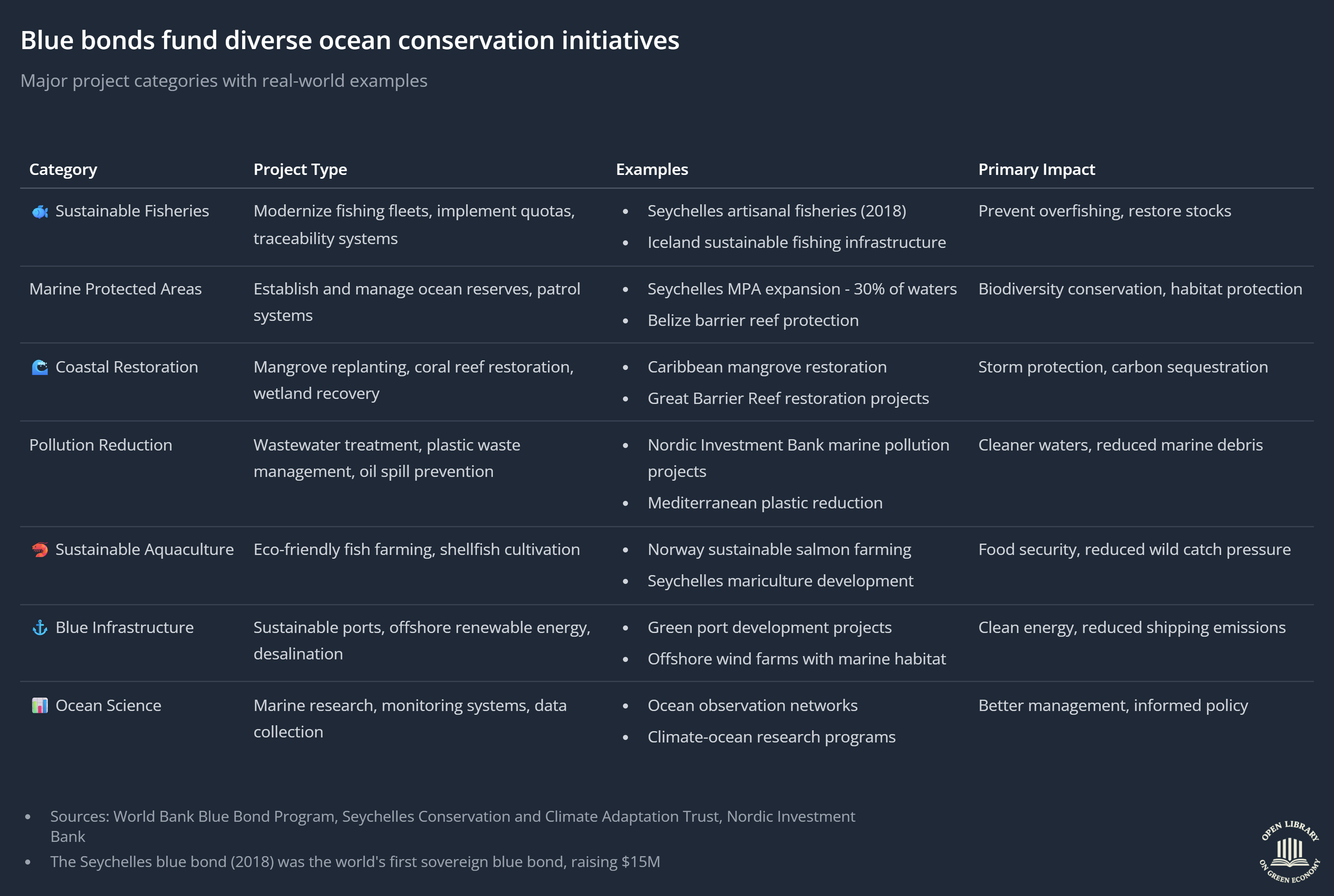

The Seychelles

The 2018 Seychelles blue bond was the first to demonstrate that capital markets could be harnessed for marine conservation. The structure of this $15 million bond offers important lessons.

The proceeds were split into two parts. A $3 million Blue Grants Fund, managed by SeyCCAT, provided grants for marine research, protection, and community-based sustainable fisheries. A larger $12 million Blue Investment Fund, managed by the Development Bank of Seychelles, provided low-interest loans to sustainable blue economy businesses such as value-added seafood processing operations and eco-friendly tourism ventures.

The bond supported the transition to the Third South West Indian Ocean Fisheries Governance and Shared Growth Program. One major outcome was the expansion of Marine Protected Areas to cover 30% of the Seychelles’ Exclusive Economic Zone. This amounts to roughly 22 million hectares of ocean. Protecting such a large area ensures that the biodiversity underpinning the nation’s tourism and fisheries sectors remains resilient to climate shocks.

Belize

In November 2021, Belize partnered with The Nature Conservancy to complete a $364 million debt conversion that reduced the national debt by 12% of GDP. The financial logic behind this transaction demonstrates how creative structuring can turn fiscal problems into conservation opportunities.

Belize held a “Superbond,” an external commercial debt trading at a deep discount of 38 cents on the dollar due to economic distress. The Nature Conservancy arranged a blue loan for Belize to repurchase $553 million of this debt at 55 cents on the dollar. This resulted in an immediate principal reduction of $189 million.

To finance the blue loan, The Nature Conservancy’s subsidiary raised capital by issuing blue bonds through Credit Suisse. These bonds received an Aa2 rating from Moody’s, a 16-notch upgrade from Belize’s sovereign rating at the time. Political risk insurance from the U.S. International Development Finance Corporation made this rating possible. The savings from refinancing created $180 million in conservation funding over 20 years. This supports the protection of 30% of Belize’s ocean, including the UNESCO-listed Belize Barrier Reef.

Corporate Sector Innovation

While sovereign bonds establish policy frameworks, corporate issuances and private banking innovations are essential for scaling the blue economy.

Notable Corporate Issuances

Corporations have used blue finance to transition their operations toward sustainability. Indorama Ventures in Thailand received a $300 million blue loan from the IFC to support plastic recycling, preventing waste from reaching the ocean. Maruha Nichiro, a Japanese seafood company, issued a 5 billion yen blue bond in 2022 to finance a land-based salmon aquaculture project. Moving aquaculture inland reduces the risk of ecosystem contamination and sea lice infestation associated with traditional open-net pens.

In October 2024, Saur issued Europe’s first benchmark corporate blue bond for a water utility. The French company raised €550 million with a 3.875% coupon. The bond was nearly four times oversubscribed, demonstrating strong investor appetite for water-themed assets.

Engaging Wealth Management Clients

In July 2025, BNP Paribas Banque Privée launched the world’s first blue bond structured specifically for private banking clients. The product raised 75 million euros within weeks, driven by client surveys showing that water and ocean issues consistently rank as top priorities for individual investors. The structure included a philanthropic component where 0.2% of the subscription amount is donated through the Dift platform to organisations like the Tara Ocean Foundation, which funds Arctic research stations.

This development suggests that retail and high-net-worth investors are eager for ocean-focused investment opportunities when products are designed to meet their preferences.

The Ecosystem of Stakeholders

Blue finance requires unprecedented collaboration between public, private, and nonprofit actors.

The Role of Multilateral Development Banks

Institutions like the World Bank and IFC serve as market anchors. They develop guidelines and taxonomies to standardise the asset class, making it easier for other participants to understand what qualifies as blue finance. They provide technical assistance to help governments identify eligible projects and establish conservation funds. They also act as cornerstone investors in new issuances, signaling confidence to private sector participants who might otherwise be hesitant.

NGOs and Scientific Organisations

Organisations like The Nature Conservancy and the World Wildlife Fund provide the scientific rigour necessary for impact verification. TNC’s Blue Bonds for Ocean Conservation strategy targets the protection of 4 million square kilometers of ocean globally. These organisations lead marine spatial planning processes, which involve local communities in deciding which ocean areas should be protected and which should remain open for sustainable fishing.

This community involvement is critical. Conservation initiatives imposed from above without local buy-in often fail. When fishers and coastal communities participate in planning, they develop ownership over outcomes and are more likely to comply with management measures.

Investors and Asset Managers

The investor base for blue bonds is diversifying. Impact investors like Calvert Impact Capital and Nuveen provided the initial capital for the Seychelles bond, demonstrating that specialised investors are willing to take on new structures. Institutional investors such as pension funds (PensionDenmark, ATP) increasingly account for nature-related risks in their portfolios. Asset managers including Fidelity and T. Rowe Price have launched dedicated blue transition bond funds and strategies, bringing ocean finance into mainstream investment products.

Technology and Data-Driven Innovation

The difficulty of monitoring marine environments has historically been a barrier to investment. Emerging technologies now provide the data needed to verify ecological outcomes.

Blockchain for Transparency

Blockchain technology is being used to enhance the lifecycle of sustainable bonds from issuance through settlement. In 2024, KfW and Intesa Sanpaolo issued digital bonds on blockchain platforms, demonstrating that distributed ledger technology can improve interoperability and enable end-to-end automation in capital markets. For blue finance specifically, blockchain can create an immutable record of how proceeds are spent, ensuring funds reach their intended environmental targets.

Advanced Monitoring Technologies

Companies like Ørsted use LiDAR (Light Detection and Ranging) to measure the flight height of seabirds and GPS tagging to monitor marine life as part of their blue bond impact reporting. This ensures that offshore wind projects deliver net-positive impacts on biodiversity rather than simply minimising harm.

Artificial intelligence processes satellite imagery and acoustic data to monitor illegal fishing and track coral reef health. These tools transform monitoring from expensive, labor-intensive field surveys into scalable, real-time systems.

Ocean Accounts

Ocean accounts represent a framework for transforming ecological metrics into financial intelligence. Think of them as natural capital balance sheets. They allow governments to quantify their economic dependency on marine assets and provide auditable metrics for bond performance. When a nation can state precisely how much economic value its coral reefs generate through tourism and coastal protection, it can make more informed decisions about whether to protect or exploit those resources.

What is Blue Carbon?

Coastal ecosystems such as mangroves, salt marshes, and seagrass meadows rank among Earth’s most effective carbon sinks. Though they cover less than 2% of the global ocean area, their sediments bury approximately 50% of all carbon stored in the ocean.

Why Blue Carbon Matters

Blue carbon ecosystems sequester carbon at rates two to four times higher than terrestrial forests. Mangroves are particularly efficient, offering the highest sequestration rates and commanding premium prices in carbon markets (around $27.80 per ton). Beyond carbon storage, these ecosystems provide coastal defense against storms, serve as nurseries for commercial fisheries, purify water, and retain soil.

Creating Self-Sustaining Financial Models

A critical synergy exists between blue bonds and blue carbon markets. Blue bonds can provide the large upfront capital required for mangrove restoration projects. Once ecosystems are restored, they generate verified carbon credits that can be sold on voluntary carbon markets. Revenue from these sales can then service the bond’s interest and principal payments, creating a self-sustaining financial model.

In 2022, the supply of blue carbon credits increased by 90%. Projects like Delta Blue Carbon in Pakistan demonstrated that buyers are willing to pay significant premiums for high-quality marine offsets. This creates a virtuous cycle where conservation becomes financially self-supporting rather than dependent on continuous public funding.

Social Equity and Blue Justice

Sustainable ocean finance must extend beyond environmental metrics to ensure social equity and the wellbeing of coastal communities.

Protecting Small-Scale Fishers

Blue finance instruments increasingly protect the livelihoods of artisanal fishers. Rare and WTW piloted a parametric insurance solution in the Philippines, where 1.9 million small-scale fishers face vulnerability to climate shocks. The insurance uses weather parameters like wind speed and sea state as triggers. If conditions prevent safe fishing for a specified number of days, direct payments are made to fishers to cover lost wages.

This provides an essential social safety net while incentivising fishers to register and participate in sustainable management practices. When fishers know they have protection against climate variability, they’re more willing to comply with catch limits and closed seasons that support long-term sustainability.

Gender Inclusion and Community Benefit-Sharing

The World Bank emphasises that scaling blue finance requires locally grounded models. This includes community benefit-sharing structures and gender inclusion targets. Women play critical roles in seafood value chains and aquaculture but often lack access to capital and training. In the Seychelles, the Blue Grants Fund explicitly targets fishers’ associations and local institutions to ensure that the transition to sustainable fisheries doesn’t marginalise local populations.

When blue finance projects include provisions for training, microloans, or cooperative development that specifically reach women and marginalised groups, they create more resilient and equitable coastal economies.

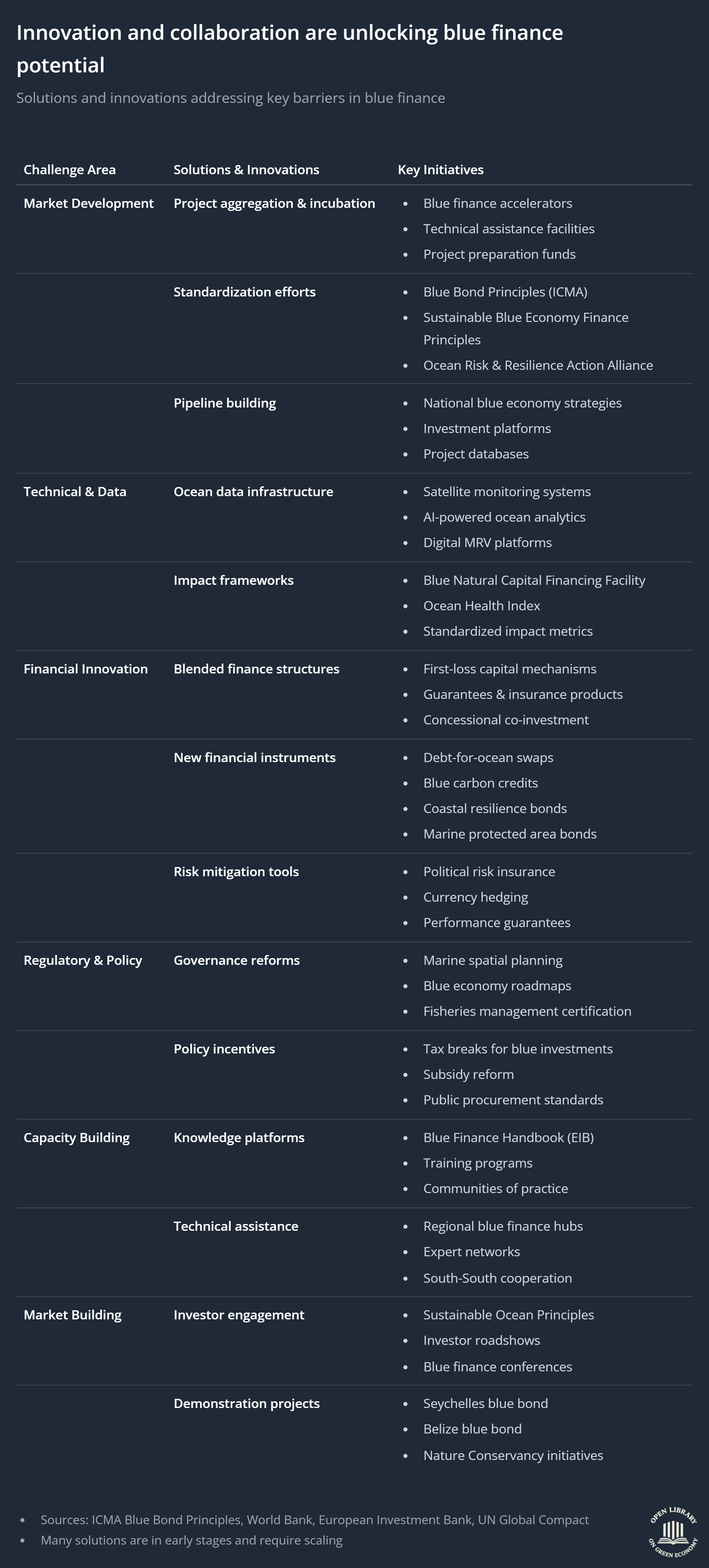

Recommendations and Research Gaps

The evolution of blue bonds from a $15 million pilot in the Seychelles to a multi-billion dollar asset class represents a big shift in sustainable finance. As the market enters 2025, the focus is transitioning from fragmented pilot projects toward coordinated, system-wide action designed to mainstream ocean sustainability into the global economy.

For Potential Issuers

Governments should move beyond standalone bond issuances and embed blue finance directly into national development plans, budgets, and regulatory frameworks. This means using a menu of context-specific options. High-debt nations might benefit most from debt-for-nature swaps like Belize’s. Countries with strong credit ratings might issue conventional sovereign blue bonds. Industrial transition might require corporate blue bonds or sustainability-linked structures.

For Investors

There is significant opportunity to capitalise on high-integrity credits, particularly those linked to blue carbon ecosystems like mangroves. These command price premiums up to 40% above standard terrestrial offsets. Investors should also advocate for ocean accounts and standardised natural capital balance sheets. These transform ecological metrics into auditable financial intelligence, reducing uncertainty and enabling better risk assessment.

For Policymakers

Accelerating alignment of standards is essential. Regional cooperation, such as through the ASEAN Green Bond Standards, can lower transaction costs and provide more prescriptive frameworks than voluntary international principles. Policies that exclude fossil-fuel-linked activities from sustainable finance definitions help maintain market integrity and prevent greenwashing.

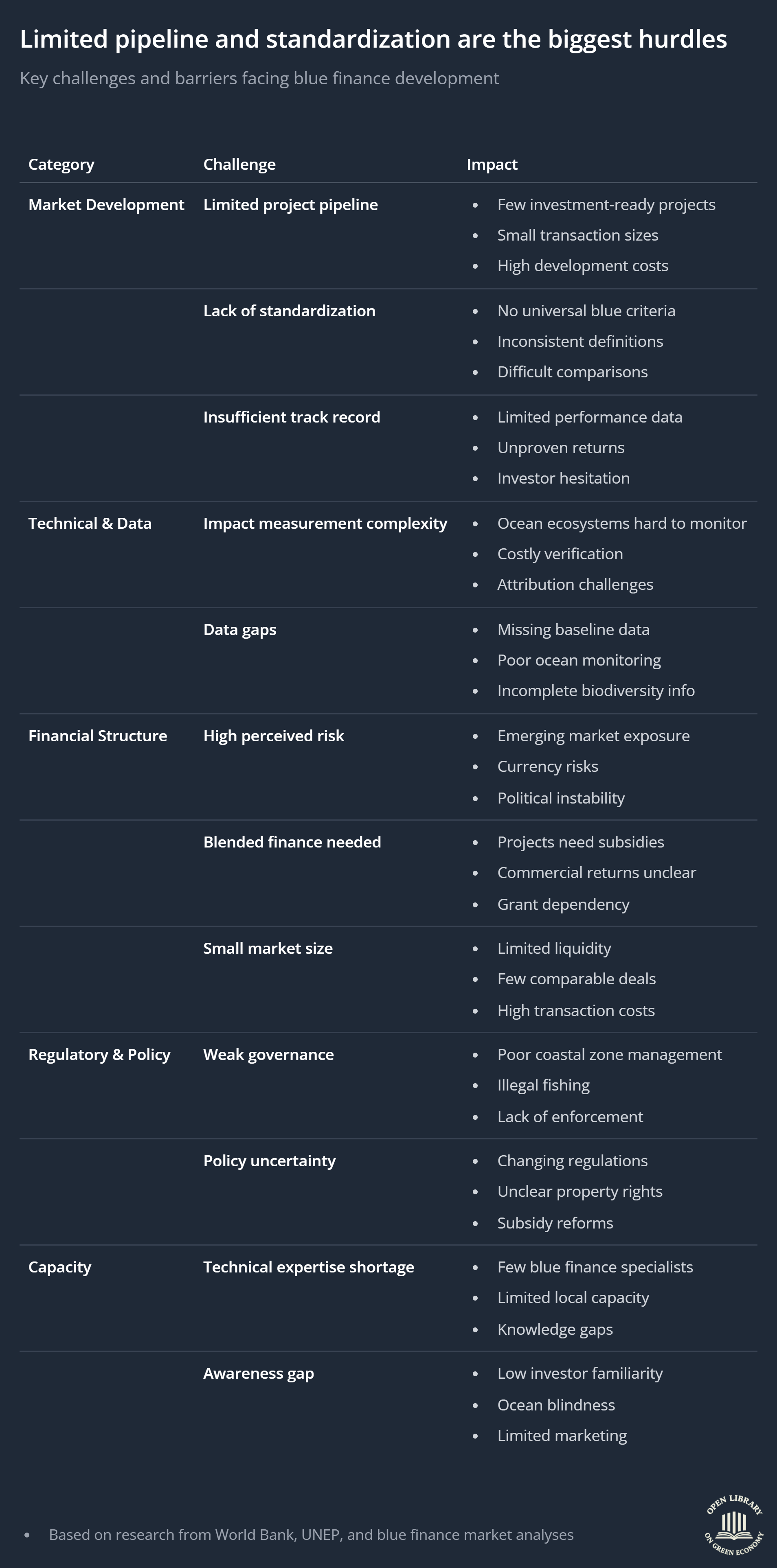

Critical Research Gaps

Several important gaps remain that impede full alignment of global markets with ocean health.

There is persistent conceptual and definitional fragmentation. Different institutions use divergent scopes for terms like “blue finance,” “ocean economy,” and “marine finance.” Research is needed to develop a unified framework that captures the connectivity of the entire hydrological cycle.

Impact measurement and verification methodologies are well-developed for coastal blue carbon but remain scientifically uncertain for open-ocean carbon enhancement. Biogenic sinks in the deep sea are legally complex due to their transboundary nature.

Many biodiverse regions, particularly in the Global South, lack good environmental baselines. Some nations have a drastic scarcity of accredited auditors compared to developed markets. This institutional capacity gap represents a bottleneck for market expansion.

Limited research exists on how large-scale blue investments impact local communities over the long term. Future studies should focus on establishing community benefit-sharing structures that ensure social legitimacy and gender inclusion. Without addressing these social dimensions, even well-intentioned projects risk failing or causing harm.

Ending Note

Blue bonds currently stand at an inflection point similar to where green bonds were a decade ago. Their ability to close the 90% funding gap for SDG 14 depends on commitment to scientific rigour, standardised data, and social equity. If current growth trajectories continue, blue bonds could mobilise up to $14 billion annually by 2030.

This would represent substantial progress but still falls short of the $175 billion needed annually. The real promise of blue bonds lies not in replacing public funding but in catalysing it. By demonstrating that ocean conservation can generate financial returns, blue bonds make the case for broader policy reforms, subsidy redirections, and the elimination of perverse incentives that currently drive ocean degradation.

The ocean economy is not separate from the global economy. It underpins food security, climate regulation, and the livelihoods of billions of people. Securing its ecological foundations through innovative finance mechanisms like blue bonds is as much an environmental need as an economic one. The question is not whether we can afford to invest in ocean health, but whether we can afford not to.