What is Green Securitisation?

Mobilising Capital for a Sustainable Future, The Mechanics of Green Securitisation, Its Transformative Potential, Challenges & Considerations, Takeaways for Participants, Infographics, etc.

The global ambition to transition towards a sustainable economy demands capital on an unprecedented scale. Traditional financing alone, while significant, often falls short of the immense investment required for green infrastructure, renewable energy projects, and sustainable urban development. This is where green securitisation emerges as a sophisticated, yet profoundly impactful, financial mechanism. It represents a vital bridge between the burgeoning demand for sustainable investments and the vast reservoirs of institutional capital seeking responsible, stable returns. More than a mere financial innovation, it is a strategic tool for scaling up green finance, taking principles of fiscal policy and applying them to private capital markets in a transformative way.

At its core, securitisation involves pooling various financial assets, converting them into marketable securities, and selling them to investors. Green securitisation applies this established technique to assets that generate environmental benefits or support climate-friendly activities. It's about taking tangible, green economic activity and packaging it into a format that broadens its appeal to a wider range of investors, effectively 'greening' the capital markets themselves.

How It Works

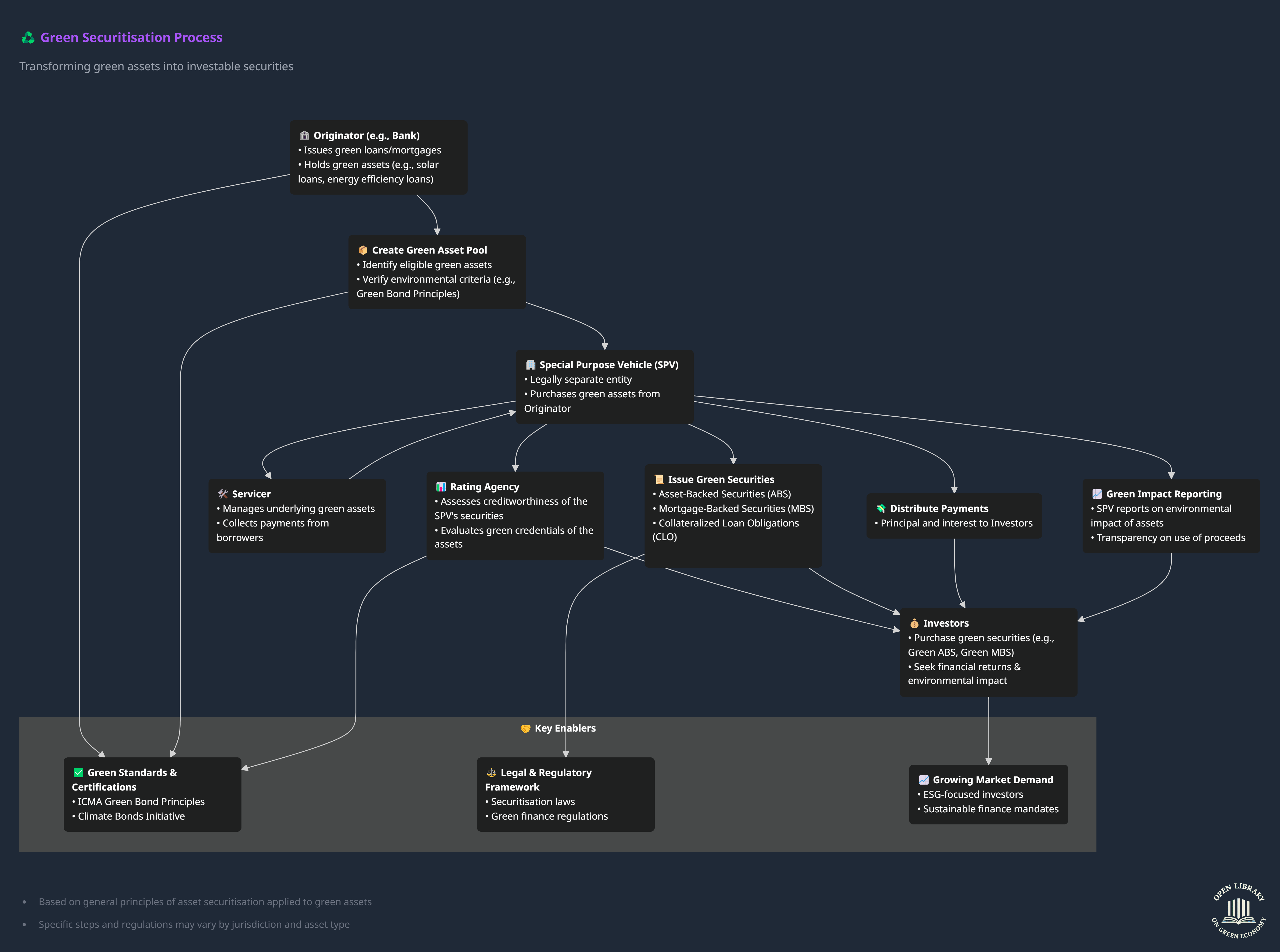

Understanding green securitisation requires a grasp of its fundamental stages and participants.

Origination of Green Assets: The process begins with the creation of financial assets linked to environmental benefits. These could be:

Green Loans: Loans provided for energy efficiency upgrades, solar panel installations, electric vehicle purchases, or sustainable agriculture.

Renewable Energy Project Debt: Debt from wind farms, solar parks, or hydro-electric facilities.

Green Mortgages: Loans for properties meeting specific environmental performance criteria.

Sustainable Infrastructure Loans: Debt related to public transport networks, sustainable water management systems, or waste-to-energy plants.

Property Assessed Clean Energy (PACE) Bonds: Special assessments on property that finance energy efficiency and renewable energy improvements, paid back through property taxes.

Pooling and Transfer: A financial institution (the 'originator') pools a collection of these green assets. These assets are then typically transferred to a Special Purpose Vehicle (SPV) – a legally distinct entity created solely for the purpose of the securitisation. This 'off-balance sheet' transfer is crucial for isolating the assets from the originator's other liabilities, enhancing investor protection.

Structuring and Credit Enhancement: The SPV then structures the pooled assets into various classes of securities, known as tranches. These tranches carry different risk and return profiles to appeal to a diverse investor base. For instance, a 'senior' tranche might have lower risk and lower returns, while a 'mezzanine' or 'equity' tranche might offer higher potential returns but also greater risk. Credit enhancements, such as over-collateralisation (padding the asset pool with more assets than required to cover the securities) or third-party guarantees, are often applied to improve the credit rating of the securities, making them more attractive.

Issuance and Marketing: The SPV issues the newly created securities (often called Asset-Backed Securities (ABS), Mortgage-Backed Securities (MBS), or more specifically, Green Bonds if the underlying assets are loans that meet green bond criteria) to investors in the capital markets. These securities are then typically listed on exchanges and traded, providing liquidity.

Servicing and Repayment: The originator or a designated servicer collects payments (e.g., loan repayments, lease payments) from the underlying green assets. These cash flows are then used to pay interest and principal to the investors holding the green securitised notes.

Why Green Securitisation Matters

The significance of green securitisation extends far beyond mere financial engineering; it addresses fundamental challenges in green finance.

Mobilising Capital at Scale: One of its primary virtues is the ability to unlock substantial institutional capital for green projects. Pension funds, insurance companies, and asset managers, often constrained by liquidity and diversification requirements, find securitised products attractive. By converting illiquid, long-term green loans into tradable securities, securitisation provides the liquidity and flexibility these large investors need. This facilitates a significant influx of capital that might otherwise remain on the sidelines.

Lowering the Cost of Capital: By pooling diversified green assets, securitisation can reduce the overall risk profile for investors compared to investing in individual green projects. This risk reduction, combined with credit enhancements, often leads to higher credit ratings for the securitised notes, which translates into lower interest rates for the issuers. A reduced cost of capital for green projects makes them more financially viable and attractive for developers.

Enhancing Liquidity: Securitisation transforms illiquid loans into tradable securities. This liquidity means investors can buy and sell these green investments more easily, making them more appealing. For originators (e.g., banks), it allows them to free up their balance sheets by selling off green loan portfolios, enabling them to make more green loans. This creates a powerful virtuous cycle of green finance.

Risk Transfer and Diversification: For originators, securitisation allows the transfer of credit risk associated with the underlying green assets to a broader investor base. For investors, these securities offer a way to diversify their portfolios with exposures to various green sectors, potentially reducing overall portfolio risk.

Standardisation and Transparency: The securitisation process often necessitates a degree of standardisation in the underlying assets and their documentation. This can improve transparency and comparability across green investments, which in turn can foster investor confidence and streamline due diligence.

Mainstreaming Green Finance: By demonstrating that green assets can be successfully packaged and sold in mainstream capital markets, green securitisation helps integrate environmental considerations into conventional finance. It normalises green investing, moving it from a niche area to a central component of global investment strategies.

Challenges and Considerations for Green Securitisation

Despite its compelling advantages, green securitisation is not without its complexities and hurdles.

Greenwashing Concerns: A significant challenge is ensuring the genuine 'green' credentials of the underlying assets. Without clear, verifiable standards and robust third-party verification, there is a risk of greenwashing, where assets are labelled 'green' for marketing purposes without delivering tangible environmental benefits. This can erode investor trust and undermine the credibility of the entire market.

Standardisation and Verification: The lack of universally agreed-upon definitions and metrics for "green" assets can complicate the pooling and rating process. Developing rigorous, transparent, and internationally recognised green criteria and independent verification processes is essential for market integrity. Initiatives by the Climate Bonds Initiative (CBI) or the International Capital Market Association (ICMA) are vital here.

Market Scale and Liquidity: While growing rapidly, the green securitisation market is still nascent compared to conventional securitisation. This can sometimes lead to lower liquidity for certain green securitised products, especially for smaller, more niche asset classes. Building sufficient deal flow and a critical mass of investors is a gradual process.

Regulatory Frameworks: Developing appropriate regulatory frameworks that support green securitisation without creating undue burdens or risks is crucial. Regulators need to balance promoting market growth with ensuring financial stability and protecting investors from misrepresentation.

Complexity: Securitisation, by its nature, is a complex financial structure. This complexity can deter some investors and requires sophisticated analytical capabilities to assess the underlying risks and cash flow profiles.

Data Availability and Quality: Reliable, granular data on the environmental performance and financial characteristics of green assets is often lacking. This makes it challenging to accurately assess risk, structure deals, and monitor impact.

Benefits of Green Securitisation

Green securitisation offers several advantages for various participants in the financial ecosystem and for the broader sustainability agenda.

For Originators (e.g., Banks):

Liquidity Creation: By selling assets off their balance sheets, originators free up capital that can then be used to originate more green loans or investments. This accelerates the flow of capital to sustainable projects.

Risk Transfer: The originator transfers the credit risk of the underlying assets to the investors, reducing their exposure and potentially freeing up regulatory capital.

Diversification of Funding Sources: It provides an alternative funding avenue beyond traditional deposits or corporate bonds, often at competitive rates due to growing investor demand for green products.

Green Branding: Issuing green securities enhances the originator's reputation as a leader in sustainable finance, attracting environmentally conscious clients and investors.

For Investors (e.g., Asset Managers, Pension Funds):

Access to Green Assets: Investors gain exposure to a diversified portfolio of green assets that might otherwise be difficult to access directly (e.g., individual small-scale solar loans).

Competitive Returns: Green ABS can offer attractive returns comparable to conventional securitised products, but with added environmental benefits.

ESG Alignment: It allows investors to meet their Environmental, Social, and Governance (ESG) mandates and sustainability goals without sacrificing financial performance.

Diversification of Portfolio: Adding green securitisation can diversify an investment portfolio, potentially reducing overall risk.

For the Green Economy:

Scale and Speed of Funding: Securitisation can funnel large amounts of private capital into green projects much faster than traditional financing methods alone, helping to close the significant funding gap for the sustainability transition.

Standardisation: The process encourages the standardisation of green project definitions and reporting, making it easier to evaluate and compare investments across the market.

Market Development: It helps develop a more mature and liquid market for green financial products, promoting innovation and reducing the cost of capital for green initiatives over time.

Transparency: Detailed reporting requirements for green securitisation enhance transparency around the environmental impact of financed projects.

Examples and Use Cases in Practice

Green securitisation has been applied across various asset classes, showing its versatility.

Solar Loan Securitisation: One of the earliest and most prevalent applications. Originators pool loans made to homeowners or businesses for installing rooftop solar panels. These cash flows, generated from loan repayments, are then securitised. For example, in 2013, SolarCity (now part of Tesla) completed one of the first publicly rated solar securitisation deals in the US, totalling approximately USD 54.4 million, paving the way for further market development (SolarCity, 2013).

Energy Efficiency Securitisation: Assets could include loans for upgrading HVAC systems, installing LED lighting, or improving building insulation in residential or commercial properties. The future energy cost savings underpin the expected cash flows.

Green Mortgage-Backed Securities (Green MBS): These pool mortgages for properties that meet certain environmental standards (e.g., certified green buildings, highly energy-efficient homes). Issuers like Fannie Mae in the US have been active in this space, issuing billions of dollars in Green MBS, incentivising the development and purchase of sustainable housing (Fannie Mae, 2024).

Electric Vehicle (EV) Loan Securitisation: As the market for EVs grows, loans taken out for EV purchases can be pooled and securitised, providing financing for the transition to cleaner transport.

PACE Bonds: A specific type of municipal bond where local governments fund energy efficiency and renewable energy improvements on private property, repaid through an assessment on the property tax bill. These assessments are then securitised.

Green Fiscal Policy for Accelerating Green Securitisation

While securitisation is a private market mechanism, green fiscal policy can play a pivotal role in catalysing and de-risking the underlying green assets, thereby accelerating the growth of green securitisation.

Targeted Subsidies and Incentives: Fiscal measures like tax credits, grants, or direct subsidies for renewable energy installations, energy efficiency upgrades, or EV purchases directly increase the volume of green assets available for securitisation. They also improve the credit quality of these underlying assets by making them more affordable or economically viable for borrowers.

"Green" Tax Incentives for Securitisation: Governments could offer tax benefits specifically for issuers or investors in certified green securitised products. This could include reduced withholding taxes on interest payments or lower corporate tax rates on income derived from such investments.

Public Procurement and Demand Creation: Government policies that mandate green standards in public procurement (e.g., only purchasing electric vehicles for public fleets) or in publicly funded housing projects create a stable demand for green technologies and services. This, in turn, generates a pipeline of green assets suitable for securitisation.

Development of Green Financial Infrastructure: Fiscal policy can support the development of green taxonomies, certification standards, and data platforms. These are not direct fiscal tools, but public funding for such infrastructure creates the enabling environment for the green securitisation market to function effectively and with integrity.

First-Loss Guarantees or Credit Enhancement: In some nascent green markets, governments or public financial institutions can provide partial credit guarantees or 'first-loss' tranches for green securitisation deals. This public support absorbs initial risks, making the deals more palatable to private investors and nurturing market confidence. This is a targeted application of public funds to de-risk private capital.

Ending Note

Green securitisation is evolving rapidly, moving beyond its initial focus on renewable energy to encompass a broader spectrum of sustainable assets, including those related to water, waste, and sustainable agriculture. As the urgency of climate action intensifies, the role of innovative financial instruments that can channel private capital effectively becomes ever more critical.

The journey of green securitisation underscores a profound lesson, that effective climate finance does not solely rely on public budgets or philanthropic gestures. Instead, it flourishes when intelligent policy design, including fiscal levers, can activate and harness the immense power of global financial markets. By understanding and strategically deploying green securitisation, we are not just funding a greener future; we are reshaping the very architecture of finance to build a more resilient and equitable world. It represents a mature step in the evolution of green finance, moving beyond niche products to mainstream financial engineering that underpins the real economy's transition.